Credit card portfolio rebalancing is the periodic realignment of your credit cards to match your actual spending habits and financial goals. Most people treat their cards as permanent fixtures, but card values shift, spending patterns change, and annual fees quietly erode returns. A well-managed portfolio targets a 2.5%–4.5% effective return for households spending $30,000–$60,000 annually. That range is achievable, but only if you review and adjust your cards at least once a year. Finja's AI-powered approach to credit card management is built on exactly this principle: your cards should work as hard as your money does.

What is credit card portfolio rebalancing?

Credit card portfolio rebalancing is the process of auditing your cards, identifying which ones still earn their keep, and making deliberate changes to close gaps or cut waste. The industry term for this practice is portfolio optimization, though "rebalancing" captures the periodic, disciplined nature of the process better than most people realize.

The goal is simple. You want your highest spending categories covered by your best-earning cards at all times. An optimal portfolio typically consists of 2 to 4 cards: one flat-rate card for miscellaneous purchases and one to three cards targeting your top spending categories. That structure keeps complexity low and reward capture high.

Category drift is the silent killer of portfolio value. It happens when your spending shifts, say from dining to groceries, but your cards stay the same. The card that once earned you 4% on restaurant meals now earns you 1% on grocery runs. Over a full year, that gap compounds into real money lost.

Rebalancing should happen at least annually. Quarterly reviews make sense if you hold cards with rotating bonus categories, since those require active management to capture the full reward rate.

When should you rebalance your credit cards?

Knowing when to act is as important as knowing how. Three clear triggers signal that a rebalance is overdue.

- A 20% or greater drop in card value. If a card's effective return falls by 20% or more, that card is no longer pulling its weight. This usually happens when a card's bonus categories no longer match your spending.

- Portal or reward rate changes of 2+ percentage points. Issuers adjust reward structures regularly. A card that offered 5% on travel may quietly drop to 3%. A shift of 2 percentage points or more is a firm trigger for review.

- Annual fees that exceed card benefits. If you cannot point to specific rewards or perks that justify a card's annual fee, that fee is a net loss. Carrying a $95 annual fee card that earns you $60 in value costs you $35 per year for the privilege of complexity.

- A new card offering meaningfully better returns. When a new card offers a significantly higher rate in a category you spend heavily in, that is a signal to reassess your current lineup.

- Lifestyle changes. A new job with a long commute, a growing family, or a shift to remote work all change where your money goes. Your cards should reflect your life as it is now, not as it was two years ago.

Pro Tip: Set a calendar reminder every january to pull 12 months of spending data from your bank or card statements. That single habit prevents category drift from quietly costing you hundreds of dollars.

The most successful rebalancers use scheduled, disciplined reviews rather than reactive changes driven by impulse or hype. Reacting to every new card launch is not a credit card strategy. It is noise.

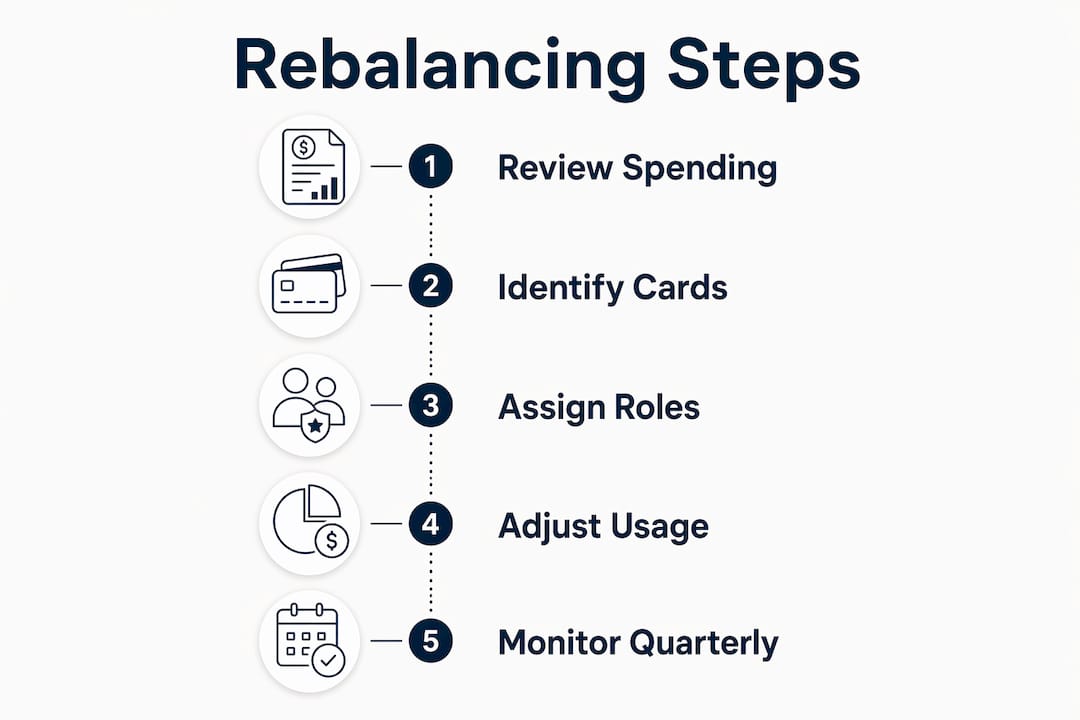

How to rebalance your credit card portfolio step by step

A structured process removes guesswork and protects your credit score throughout the rebalance.

-

Pull 12 months of spending data. Export statements from every card and bank account. Categorize spending into buckets: groceries, dining, travel, gas, subscriptions, and general purchases. This spending forensics step is non-negotiable. Selecting cards based on desired spending rather than actual spending is the most common mistake people make.

-

Map your current cards to your spending categories. List every card you hold, its reward rate per category, and its annual fee. Identify which categories are covered well and which are earning only 1% because no card in your wallet targets them.

-

Identify redundant or underperforming cards. Look for cards that duplicate coverage. If two cards both offer 3% on dining, one is redundant. Also flag any card whose annual fee exceeds its measurable benefit. These are candidates for downgrading or closing.

-

Decide: close, downgrade, or keep. Closing a card reduces your available credit and can hurt your credit utilization ratio. Downgrading a card to a no-fee version preserves your account age and credit history while eliminating the annual fee. Downgrading is almost always the better move for older accounts.

-

Identify gaps and select replacement cards. Once you know which categories are uncovered, research cards that fill those gaps. Aim for 60%–75% category coverage at 4%–6% reward rates, with one flat-rate card as a fallback for everything else.

-

Space new applications 3–6 months apart. Applying for multiple cards in a short window triggers multiple hard inquiries and can signal credit risk to lenders. Space applications to protect your score and give yourself time to meet welcome bonus spending requirements without stress.

-

Time applications to peak welcome bonuses. Issuers periodically raise welcome bonuses well above their standard offers. Waiting for a peak bonus often yields 10x or greater returns compared to normal spending rewards. Patience here is a genuine financial advantage.

-

Assign clear roles to every card. Each card in your wallet should have one job. Card A handles groceries. Card B handles travel. Card C is the flat-rate fallback. Written role assignments reduce the mental load of deciding which card to use at checkout.

Pro Tip: Use a simple spreadsheet with columns for card name, annual fee, reward rate per category, and estimated annual value. Update it during each review. The act of writing it down forces clarity that mental accounting never achieves.

Common pitfalls in credit card portfolio management

Even disciplined rebalancers fall into traps that quietly undermine their returns.

- Lifestyle drift. Continuing to use cards out of habit despite losing rewards is the single biggest barrier to effective rebalancing. Muscle memory is not a credit card strategy.

- Category overlap. Holding multiple cards that reward the same spending category is inefficient. It complicates your wallet and dilutes the mental clarity that makes a good portfolio work.

- Chasing minor rate changes. Applying for a new card to capture an extra 0.5% on a low-spend category costs more in time, credit inquiries, and mental load than it earns. Focus on meaningful value gaps, not marginal improvements.

- Ignoring issuer restrictions. Chase's 5/24 rule, for example, blocks approval for most Chase cards if you have opened five or more cards in the past 24 months. Lifetime welcome bonus limits on certain cards also affect rebalancing strategy. Knowing these rules before you apply saves wasted hard inquiries.

- Excessive card churn. Most people overestimate the value of adding more cards while underestimating the mental and security risks of complexity. A wallet of eight cards is not a portfolio. It is a liability.

- Closing old accounts impulsively. Closing a card with a long history shortens your average account age and reduces available credit. Both effects can lower your credit score meaningfully.

The fix for most of these pitfalls is the same: treat your credit cards like an investment portfolio, with discipline, scheduled reviews, and clear rules for when to act.

How credit card rebalancing compares to investment portfolio rebalancing

Both practices share the same core logic: realign your holdings to your goals when drift occurs. The mechanics differ in important ways.

| Dimension | Investment portfolio | Credit card portfolio |

|---|---|---|

| Core action | Buy and sell assets | Prune cards and reassign spending roles |

| Trigger | Target allocation drift | Category drift, fee imbalance, rate changes |

| Frequency | Annually or on threshold | Annually, quarterly for rotating categories |

| Risk of inaction | Portfolio grows misaligned with risk tolerance | Fees accumulate, rewards erode |

| Primary goal | Long-term wealth growth | Reward capture and cost reduction |

The key difference is that credit card rebalancing involves pruning and role assignment rather than selling assets. You are not liquidating positions. You are deciding which cards earn a place in your wallet and what job each one does.

Investment rebalancing also carries tax implications that credit card rebalancing does not. That makes credit card rebalancing lower stakes in one sense, but the behavioral discipline required is identical. Both reward patience and punish reactive decision-making.

The portfolio thinking model also reduces cognitive load. When every card has a defined role, you stop second-guessing at checkout. That mental clarity is a real, underrated benefit of a well-structured credit card strategy.

Key takeaways

Credit card portfolio rebalancing produces the best results when you combine annual spending analysis, clear card roles, and disciplined timing on new applications.

| Point | Details |

|---|---|

| Define card roles clearly | Assign each card one spending category to reduce complexity and maximize reward capture. |

| Review at least annually | Pull 12 months of spending data every year to catch category drift before it costs you. |

| Downgrade before closing | Product changes preserve account age and credit history while eliminating annual fees. |

| Wait for peak bonuses | Timing new applications to elevated welcome offers produces far greater long-term value. |

| Keep the portfolio small | A 2–4 card portfolio with 60%–75% category coverage outperforms a bloated wallet of eight or more cards. |

What I've learned from watching people rebalance their cards

Most people who struggle with their credit card portfolios are not making big, obvious mistakes. They are making small, quiet ones. They keep a card because canceling it feels like admitting defeat. They apply for a new card because a friend mentioned it, not because their spending data supports it. They check their reward balances but never their effective return rate.

The annual review ritual is the single most underrated habit in personal finance. Not because it is complicated, but because it forces you to confront the gap between what you think your cards earn and what they actually earn. That gap is almost always larger than expected.

My honest recommendation: simplify before you add. Most people I have seen improve their financial health through better card management did it by cutting cards, not adding them. Three well-chosen cards beat eight mediocre ones every time. The mental load of managing a large wallet is a real cost that never shows up in a reward statement.

Patience is also genuinely undervalued. Waiting three months for a better welcome bonus is not passive. It is the highest-return move available to most cardholders. The discipline to wait is what separates people who extract real value from their cards from those who just collect them.

— Grace K.

How Finja helps you rebalance your credit card portfolio

Managing a credit card portfolio manually takes time, spreadsheets, and a level of financial attention most people cannot sustain consistently.

Finja's AI credit card coach analyzes your spending data, identifies category gaps, flags cards where fees exceed benefits, and surfaces personalized card recommendations timed to your financial goals. It handles the spending forensics that most people skip, which is the step that determines whether a rebalance actually improves your returns. For anyone managing multiple credit cards and looking to reduce both cost and complexity, Finja turns a once-a-year manual audit into an ongoing, guided process.

FAQ

What is credit card portfolio rebalancing in simple terms?

Credit card portfolio rebalancing is the process of reviewing your cards and adjusting which ones you use, keep, or close so your spending always earns the best possible rewards. It should happen at least once a year.

How often should I rebalance my credit card portfolio?

Annual rebalancing is the minimum standard. Quarterly reviews make sense if you hold cards with rotating bonus categories that require active management to capture full reward rates.

What triggers a credit card rebalance?

The three main triggers are a 20% or greater drop in a card's effective value, a reward rate change of 2 or more percentage points, and an annual fee that exceeds the card's measurable benefits.

Should I close cards when rebalancing?

Closing cards is usually the last resort. Downgrading to a no-fee version of the same card preserves your account age and credit history, which protects your credit score while eliminating the annual fee burden.

How is credit card rebalancing different from investment rebalancing?

Investment rebalancing involves buying and selling assets to restore a target allocation. Credit card rebalancing involves pruning cards and reassigning spending roles, with no tax implications and a focus on reward capture rather than wealth growth.