Credit card financial modeling is defined as the quantitative framework used to estimate the profitability, risks, and cash flows tied to credit card portfolios. Banks and issuers build these models to forecast revenue and losses. But the same logic applies directly to you as a cardholder. Understanding how issuers think about your account gives you a real edge in choosing cards, managing balances, and capturing rewards without paying for them twice. This guide breaks down the core mechanics of financial modeling for credit cards and translates them into decisions you can act on today.

What is credit card financial modeling and why does it matter?

Credit card financial modeling is the practice of building data-driven frameworks to forecast revenue, costs, risk, and net profitability across a credit card portfolio. The industry term used by analysts and product managers is credit card portfolio modeling, though the concepts apply equally to individual account analysis. Issuers use these models to set interest rates, approve credit lines, and design rewards programs. When you understand the model, you understand why your card behaves the way it does.

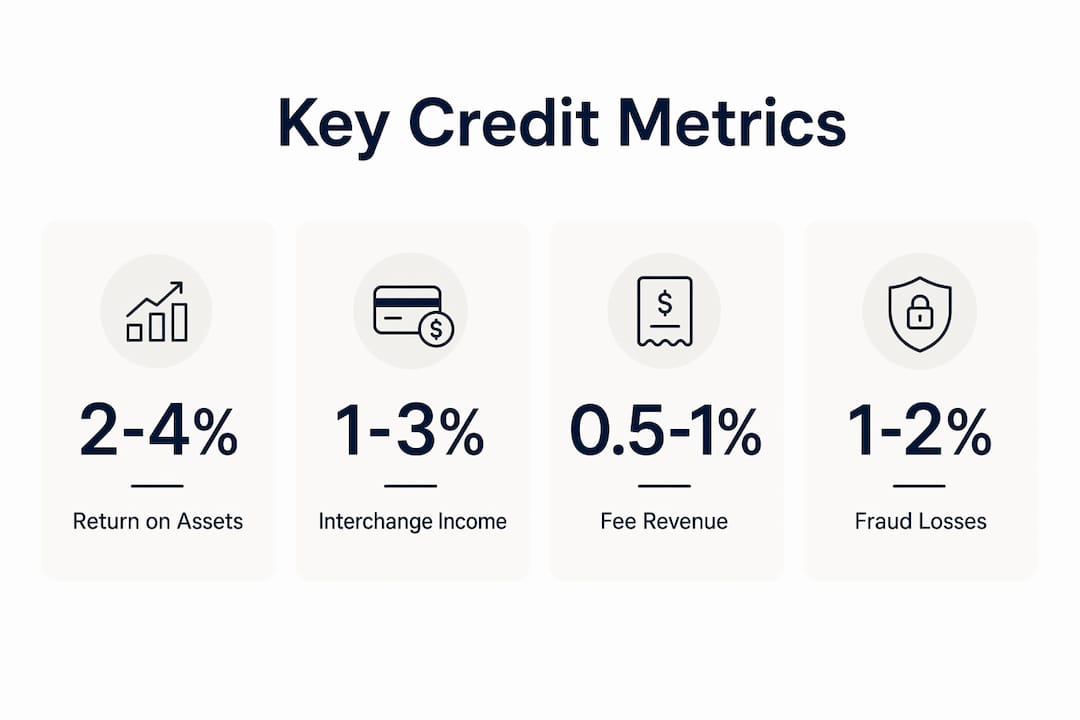

Healthy credit card portfolios target a 2–4% Return on Assets (ROA), with interchange revenues typically ranging from 1.3% to 1.8% of spend. That benchmark tells you exactly how thin the margins are. Rewards programs consume 25–50 basis points of that revenue, which explains why premium rewards cards charge annual fees to stay profitable.

The three main stakeholders in any credit card model are issuers, borrowers, and portfolio managers. Each group cares about a different output. Issuers watch ROA and net card income. Borrowers care about interest costs and credit health. Portfolio managers track loss rates and acquisition efficiency. Knowing which side of the model you sit on changes how you read every offer that lands in your mailbox.

What are the fundamental metrics in credit card financial models?

Credit card models are built on a small set of metrics that interact in predictable ways. Mastering these gives you a framework for evaluating any card or offer.

Revenue metrics include interchange income, interest income, and fee revenue. Interchange is the percentage of each transaction paid by the merchant's bank to the card issuer. Interest income comes from revolving balances. Fee revenue covers annual fees, late fees, and cash advance charges.

Cost metrics include rewards and loyalty costs, customer acquisition costs (CAC), fraud losses, and the cost of funds. Variable costs average about $160 per account annually, covering defaults and cost of funds. That figure sets the floor for what an issuer needs to earn from each account to break even.

Credit risk parameters are the backbone of any loss forecast. Credit risk modeling relies on three core inputs: Probability of Default (PD), Exposure at Default (EAD), and Loss Given Default (LGD). Together, these three figures produce the expected credit loss for any segment of cardholders.

| Metric | What it measures | Typical range |

|---|---|---|

| Return on Assets (ROA) | Net profitability per dollar of receivables | 2–4% |

| Interchange revenue | Revenue per dollar spent | 1.3–1.8% of spend |

| Rewards cost | Cost of points, miles, and cashback | 0.25–0.50% of spend |

| Variable cost per account | Defaults plus cost of funds | ~$160/year |

| Probability of Default (PD) | Likelihood a borrower misses payment | Varies by segment |

Pro Tip: If a card's rewards rate exceeds 1.8%, the issuer is almost certainly funding the gap through your annual fee or through interest from revolvers. Knowing this helps you pick the right card for your spending profile.

Which modeling techniques are used for credit card analysis?

Credit card analysis methods range from simple breakeven calculations to machine learning models running on millions of transactions in real time. The technique used depends on the question being answered.

Breakeven and contribution margin analysis is the starting point. An issuer calculates the contribution margin by subtracting variable costs from revenue per account. Marketing costs for a single card product launch can reach $12 million, which means a new card needs a large, profitable cardholder base to recover fixed costs. The payback period on that spend drives every pricing and targeting decision.

Customer segmentation splits cardholders into behavioral groups. The two most important are transactors and revolvers. Transactors pay their balance in full each month. Revolvers carry a balance and pay interest. Spend margin analysis shows that transactors can be net-negative customers because their rewards costs exceed the interchange revenue they generate. Revolvers subsidize the entire rewards ecosystem.

Machine learning models handle fraud detection, churn prediction, and dynamic credit line management. Techniques like XGBoost gradient boosting and Long Short-Term Memory (LSTM) neural networks process behavioral patterns that no human analyst could track manually.

Stress testing models the impact of regulatory changes. Regulatory pressure to cap APRs forces issuers to build sensitivity models that stress-test impacts on net income and equity valuation. When Congress debates an interest rate cap, issuers run these models to forecast how their portfolio economics change.

Here is how the main modeling approaches compare by purpose:

| Technique | Primary purpose | Complexity |

|---|---|---|

| Breakeven / contribution margin | Profitability per account | Low |

| Customer segmentation | Behavioral targeting | Medium |

| XGBoost / LSTM models | Fraud detection, churn | High |

| Stress testing | Regulatory scenario analysis | High |

| Payback period analysis | Acquisition cost recovery | Low |

Pro Tip: When evaluating a signup bonus, apply the payback period concept yourself. If the bonus is worth $500 but the card's annual fee is $95 and you would not naturally spend enough to earn ongoing rewards, the issuer's model says you are unprofitable. That usually means the card is not a good fit for your habits either.

How do risk factors and fraud detection shape financial projections?

Risk is not a footnote in credit card modeling. It is a primary driver of profitability, and fraud alone can erase an entire year of interchange revenue.

Credit card fraud caused losses exceeding $32 billion globally in 2021. That figure represents a direct hit to net card income for every issuer in the market. Fraud losses reduce the ROA that models are built to protect, which is why fraud detection is treated as a financial modeling problem, not just a security problem.

The core challenge in fraud detection is class imbalance. Over 99.8% of transactions are legitimate. A model that simply labels every transaction as "not fraud" would be technically accurate but financially catastrophic. Specialized methods like SMOTE (Synthetic Minority Over-sampling Technique) and cost-sensitive learning address this by making the model treat a missed fraud event as far more costly than a false positive. The result is detection accuracy above 99% on real-world datasets.

Key risk modeling techniques used in credit card portfolios include:

- Real-time anomaly detection: Flags transactions that deviate from a cardholder's behavioral baseline within milliseconds.

- Behavioral scoring: Assigns a risk score to each account based on payment history, utilization trends, and spending patterns.

- Collection nudges: AI-driven alerts sent to cardholders who show early signs of repayment stress, reducing default rates before they materialize.

- Churn prediction models: Identify cardholders likely to close their account, triggering retention offers before the relationship ends.

AI applications in credit card management now span underwriting on alternative data, dynamic rewards personalization, anomaly detection, and collection nudges. Each application feeds back into the financial model, updating projections in real time rather than quarterly.

How can you apply credit card modeling insights to personal finance?

The same logic that drives issuer profitability models can guide your personal credit decisions. You just need to read the model from the other side of the table.

-

Know your cardholder profile. If you pay your balance in full every month, you are a transactor. Issuers earn less from you, which means they need your annual fee to justify the relationship. Choose cards where the rewards clearly exceed the fee, because the issuer's model already assumes you will not pay interest.

-

Evaluate acquisition offers with payback logic. Signup bonuses that exceed first-year gross margin signal potential unprofitability for the issuer without long-term retention. From your side, a generous signup bonus is only valuable if you can meet the spending requirement without changing your normal behavior. Forced spending to hit a bonus threshold often costs more than the bonus is worth.

-

Understand how utilization affects your risk score. Issuers use EAD as a core risk input. High utilization raises your EAD, which raises your modeled risk, which can trigger credit line reductions or rate increases. Keeping utilization below 30% of your available credit directly reduces your modeled risk profile.

-

Use rewards programs as a transactor, not a revolver. The moment you carry a balance, interest charges eliminate any rewards value. A 20% APR on a $1,000 balance costs $200 per year. No cashback program returns 20%.

-

Treat your credit card as a dynamic financial tool. Credit card product managers view cards as evolving platforms emphasizing AI-driven nudges and real-time behavior monitoring. The card you hold today is being repriced and re-evaluated continuously based on your behavior. Active management of your account, including on-time payments, controlled utilization, and strategic rewards redemption, directly improves the model's view of your account.

Pro Tip: Request a credit line increase every 12–18 months if your payment history is clean. A higher limit with the same balance lowers your utilization ratio, which improves your risk profile in the issuer's model and can lead to better rate offers.

Key takeaways

Credit card financial modeling gives you a framework to make better credit decisions by understanding exactly how issuers measure profitability and risk on your account.

| Point | Details |

|---|---|

| ROA is the core profitability target | Healthy portfolios target 2–4% ROA; rewards and fees are calibrated to hit that number. |

| Transactors and revolvers are priced differently | Transactors often generate negative margins; revolvers subsidize rewards programs through interest. |

| Fraud modeling is a financial priority | $32B+ in annual fraud losses make detection models as important as revenue forecasts. |

| Payback period logic applies to you | Evaluate signup bonuses and annual fees using the same payback period logic issuers use. |

| Utilization directly affects your risk model | Keeping utilization below 30% lowers your modeled EAD and improves your credit profile. |

Credit cards are more dynamic than most people realize

Most cardholders treat their credit card as a static product. They pick a card, use it, and pay the bill. What they miss is that the issuer is running a live financial model on their account every single day.

I have spent years watching people leave real money on the table because they did not understand the economics behind their card. The most common mistake is treating a high-rewards card as free money. Those rewards are funded by interchange, annual fees, and, most importantly, by the interest paid by revolvers. If you carry a balance even once, you have crossed from the profitable side of the model to the expensive side.

The second misconception is that credit card offers are static. They are not. Issuers reprice accounts, adjust credit lines, and modify rewards structures based on real-time behavioral data. A cardholder who pays on time, keeps utilization low, and spends consistently is a valuable account. That account gets better retention offers, proactive limit increases, and lower risk-based pricing over time.

The shift toward AI-driven personalization makes this even more pronounced. Models now update faster than any human analyst could manage. Your behavior this month influences your account terms next month. That is not a threat. It is an opportunity. Cardholders who understand the model and manage their behavior accordingly get the best outcomes the issuer's economics can support.

The practical takeaway is simple. Read your credit card like a financial instrument, not a payment method. Know your profile, know your costs, and make decisions that put you on the right side of the model.

— Grace K.

Finja can put these insights to work for you

Understanding credit card financial modeling is one thing. Applying it across multiple cards, balances, and rewards programs is another challenge entirely.

Finja is an AI-powered credit card management platform built for cardholders who want to make better decisions with the cards they already have. Finja analyzes your spending patterns, payment behavior, and card economics to surface personalized recommendations that reflect the same logic issuers use in their own models. Whether you want to reduce interest costs, improve your credit health, or get more value from your rewards, Finja translates financial modeling principles into clear, specific guidance for your situation.

FAQ

What is credit card financial modeling in simple terms?

Credit card financial modeling is the process of using data and math to forecast the revenue, costs, and risks tied to credit card accounts. Issuers use it to set rates and design rewards; cardholders can use the same logic to choose better cards and manage balances.

What are the three core credit risk parameters in card modeling?

The three core parameters are Probability of Default (PD), Exposure at Default (EAD), and Loss Given Default (LGD). Together, they produce the expected credit loss for any group of cardholders.

Why do transactors sometimes cost issuers money?

Transactors pay their balance in full each month, so issuers earn no interest from them. When rewards costs exceed interchange revenue on those accounts, the issuer runs a negative margin on the relationship.

How does fraud detection connect to financial modeling?

Fraud losses directly reduce net card income and ROA. Issuers treat fraud detection as a financial modeling problem, using machine learning techniques like XGBoost and SMOTE to minimize losses that would otherwise erode portfolio profitability.

How can I use credit card modeling logic to improve my finances?

Keep utilization below 30% to lower your modeled risk profile, pay in full to avoid interest that wipes out rewards value, and evaluate signup bonuses using payback period logic before applying for a new card.