Managing multiple credit cards often means tracking different balances, due dates, and payment strategies across several apps. Many credit card management tools only provide isolated account views, and skip real AI-driven payment guidance. This comparison outlines pricing, payment automation, and guidance features so individuals can pick a credit card management software that fits their need for unified card tracking and actionable payment advice.

Table of Contents

Finja

At a Glance

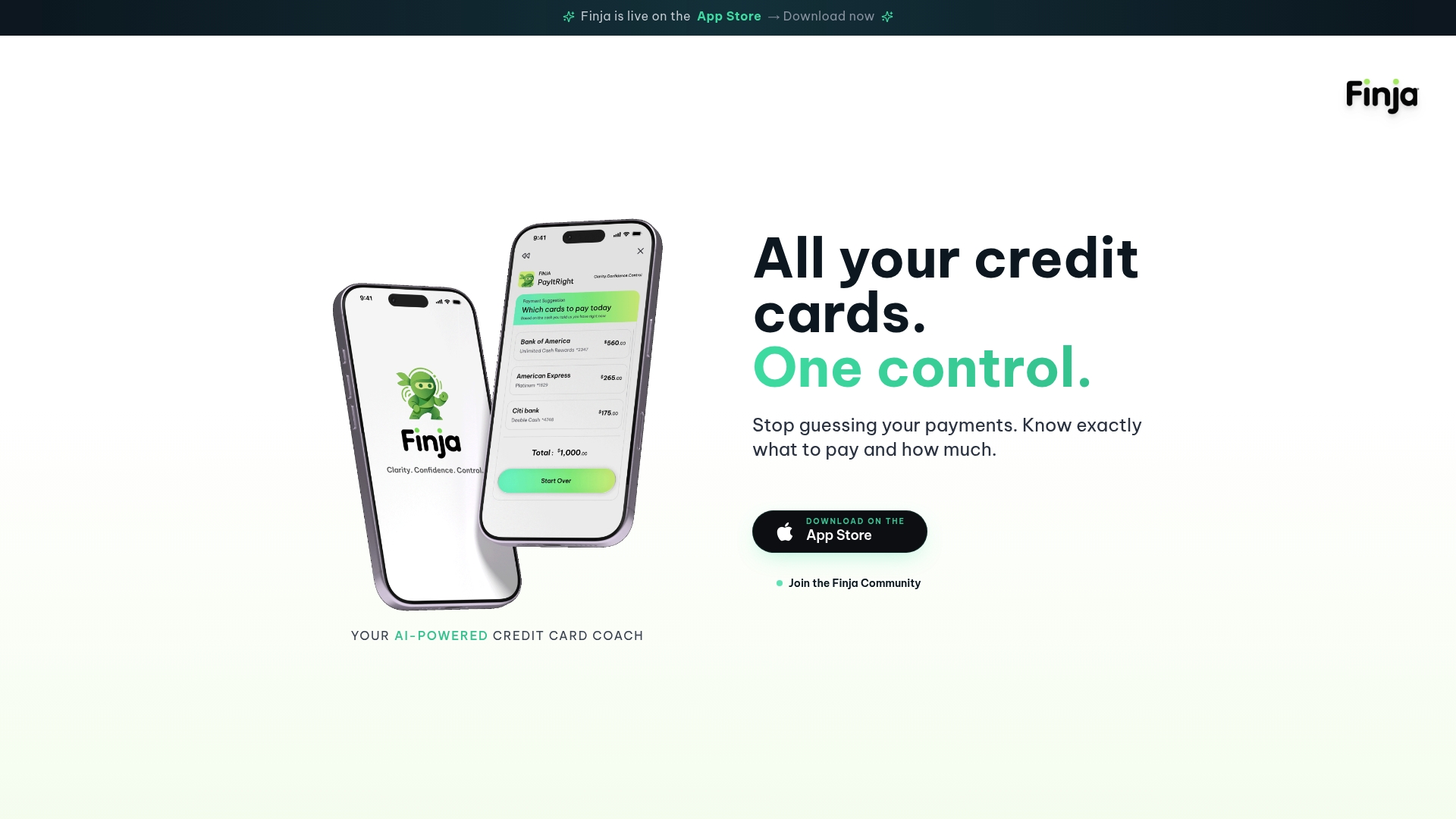

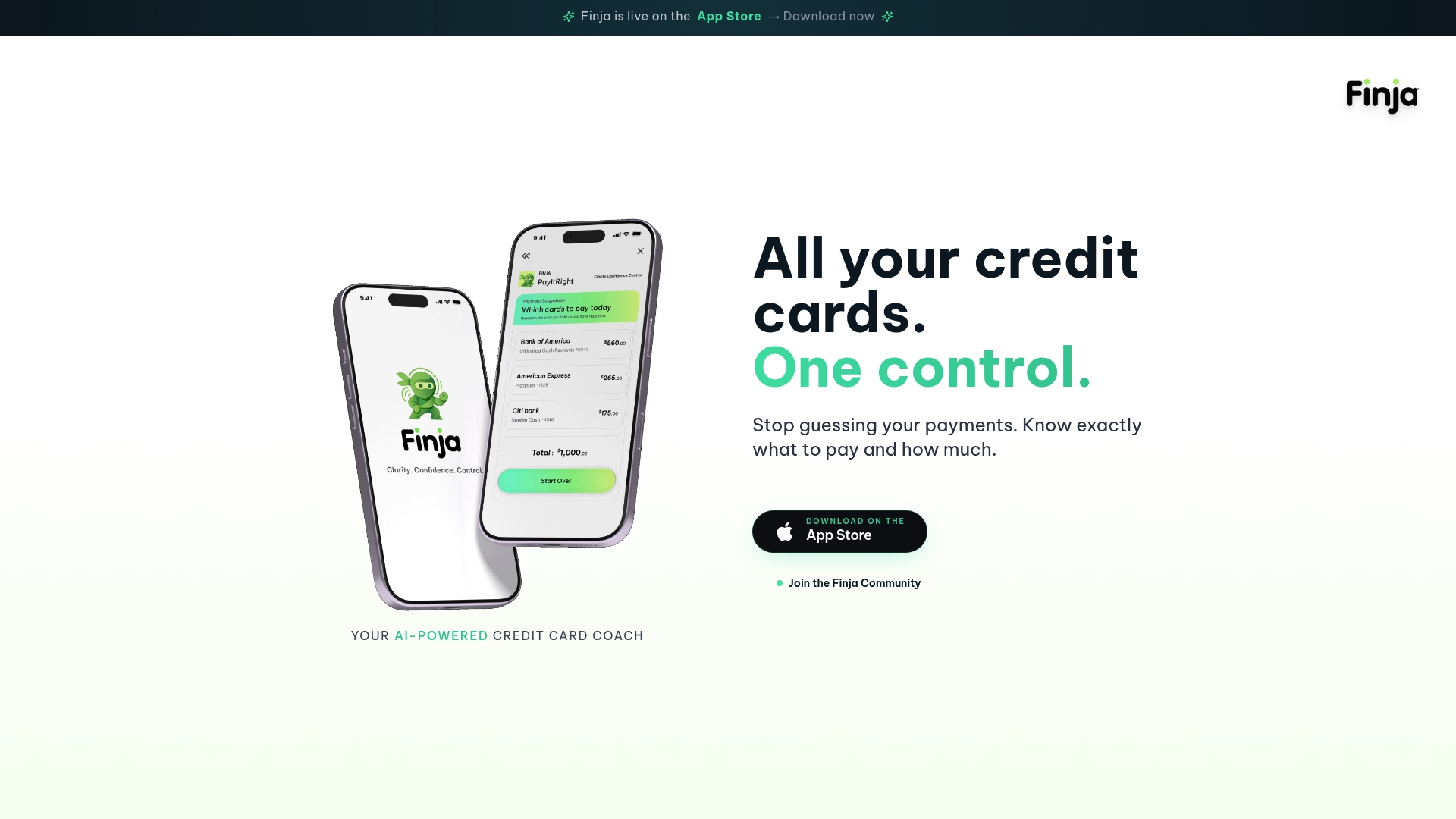

See all credit card balances in one view. That single-screen balance snapshot removes the need to open several apps to check amounts and due dates. The app pairs that visibility with AI suggestions so you know which card to pay and when.

Core Features

Finja shows consolidated card balances while offering AI-powered payment recommendations that suggest amounts and timing to reduce interest. The app lets you set spending limits by category and includes a personalized credit knowledge quiz to build understanding. Cards link securely using bank-grade encryption for account connections.

Key Differentiator

Finja centers its value on AI-driven personalized payment guidance combined with a full credit overview in one place. The combination means recommendation logic sees your entire card picture before suggesting a payment. That integrated view changes how payment decisions are generated compared with single-card tools.

Pros

A single balance view cuts the friction of checking multiple accounts, so you spot due dates and total exposure quickly. The AI suggestions adapt to your balances and payment schedule and aim to lower avoidable interest through recommended payment timing. Spending limits give active control over categories like dining and shopping, and the credit quiz helps you learn concepts without heavy finance jargon.

Cons

- Limited transparency on subscription pricing and premium features.

Who It's For

Finja fits people who hold two or more credit cards and want clearer, actionable payment guidance. It works well for someone who wants to prioritize credit health over rewards chasing. The app appeals to readers who prefer simple recommendations to manual spreadsheet calculations.

Unique Value Proposition

Daily AI payment suggestions that consider every linked card let you prioritize payments with fewer guesses. That practical guidance reduces the chance of missed minimums and can help you shrink interest costs over time. For someone juggling cards, this replaces manual math with a rule set tuned to your balances and due dates.

Real World Use Case

A person links three credit cards, then receives a daily payment recommendation focused on minimizing interest and covering nearest due dates. They set a spending limit for dining and reduce impulse charges that month. The clear balance screen and recommended payment schedule prevent missed payments.

Pricing

The website does not list specific subscription tiers or starting prices. The publicly available content describes core features but does not specify premium feature fees or trial terms.

Website: https://myfinja.com

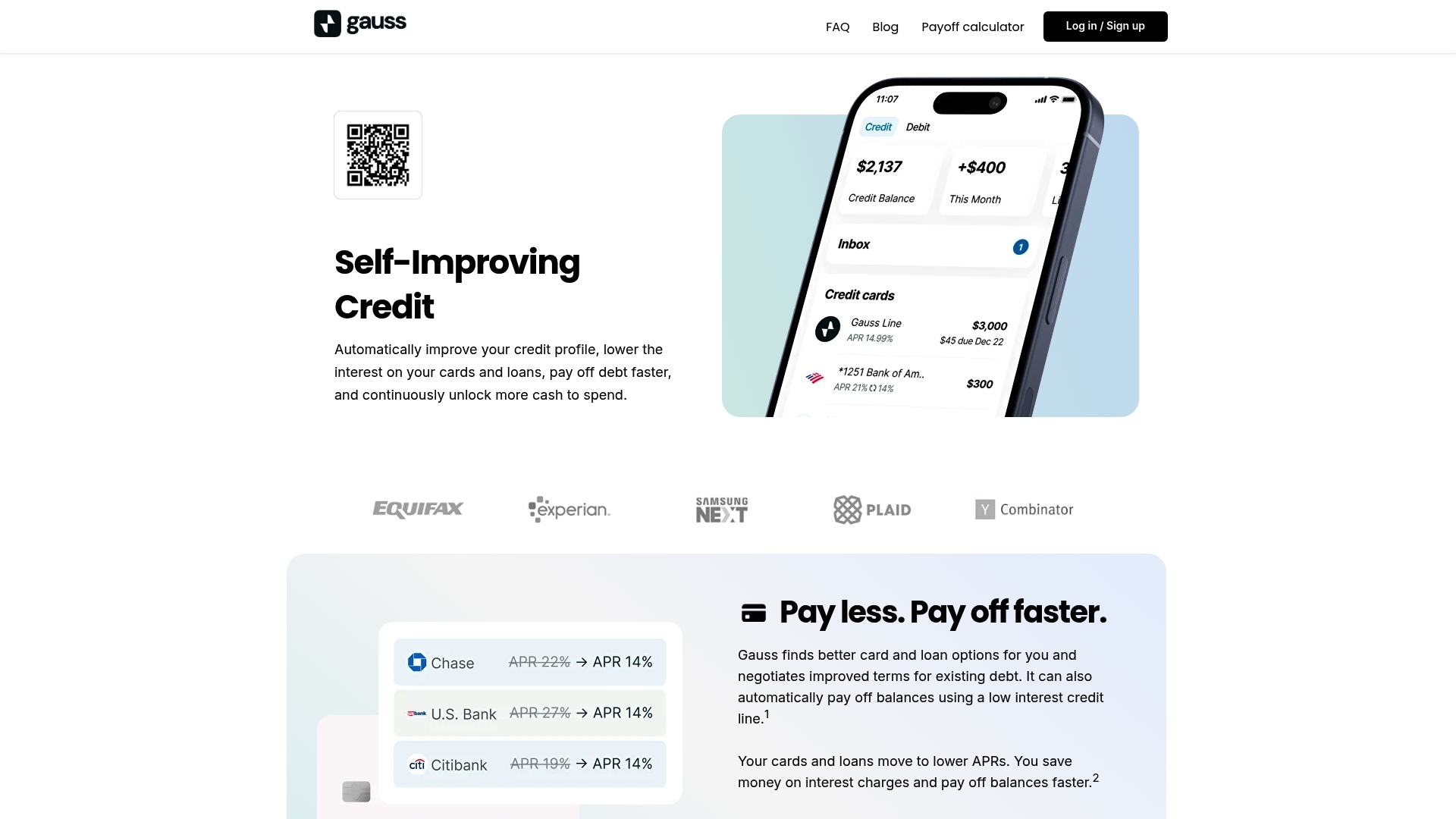

Gauss Total Credit Manager

At a Glance

The vendor advertises a starting membership fee of $4.99/month for core services. Gauss combines AI driven debt negotiation, credit report tracking, and automated balance transfers in a single app. It targets people who manage multiple credit accounts and want routine fee free credit management on web and mobile apps.

Core Features

Gauss uses AI driven debt negotiation to request lower interest rates and improved terms, and it pairs that with automatic balance transfers to lower interest credit lines. The app tracks credit reports and suggests actions to improve credit profiles while consolidating cards and loans into one dashboard. Core services are presented as having no hidden fees with additional charges limited to certain credit products.

Key Differentiator

Gauss stands out for automated negotiation that runs without extensive manual work and without requiring credit checks for its improvement process. The platform continuously monitors accounts and negotiates on an ongoing basis rather than offering one time interventions. That focus on persistent negotiation plus automated transfers narrows the effort you must put into lowering interest costs.

Pros

Gauss helps reduce interest costs and accelerates payoff by automating transfers and negotiation, which lowers monthly interest expense and frees cash for principal payments. The app supports multiple credit accounts and loan types in the same place, so you do not juggle separate portals. Core features are available on web, Android, and iOS and the vendor states there are no hidden fees for those core services.

Cons

- Buyer reviews indicate limited free features, with most credit improvements requiring paid plans.

- Effectiveness depends on the user credit profile and recent account activity, so results vary by individual circumstances.

- Some features may be restricted by location, state rules, or the specifics of a person credit history.

When It May Not Fit

Gauss may not fit people who have little or no credit history since the platform needs active accounts to negotiate and track improvements. It is not a bank and does not provide direct loans or deposit accounts, so you still need a banking partner for payments. If you need time tracking, cash management, or nested bank services, Gauss will leave gaps in those workflows.

Who It's For

This product fits active credit users who carry multiple credit cards or loans and who want routine help lowering borrowing costs. It suits people willing to rely on an app to handle negotiation and transfers rather than doing that work themselves. It also works for those who prefer a single dashboard for monitoring credit health across accounts.

Real World Use Case

A person with three credit cards and a personal loan uses Gauss to move balances to lower rate lines and to run negotiation cycles on high rate cards. The app monitors credit reports and alerts when a new negotiation opportunity appears. Over months the user focuses payments on principal while the app tries to lower interest costs.

Pricing

The vendor advertises a membership that starts at $4.99/month. Core credit management services are described as having no hidden charges, while extra fees may apply for certain third party credit products or special transactions. That starting price is the listed entry point for membership.

Website: https://gauss.money

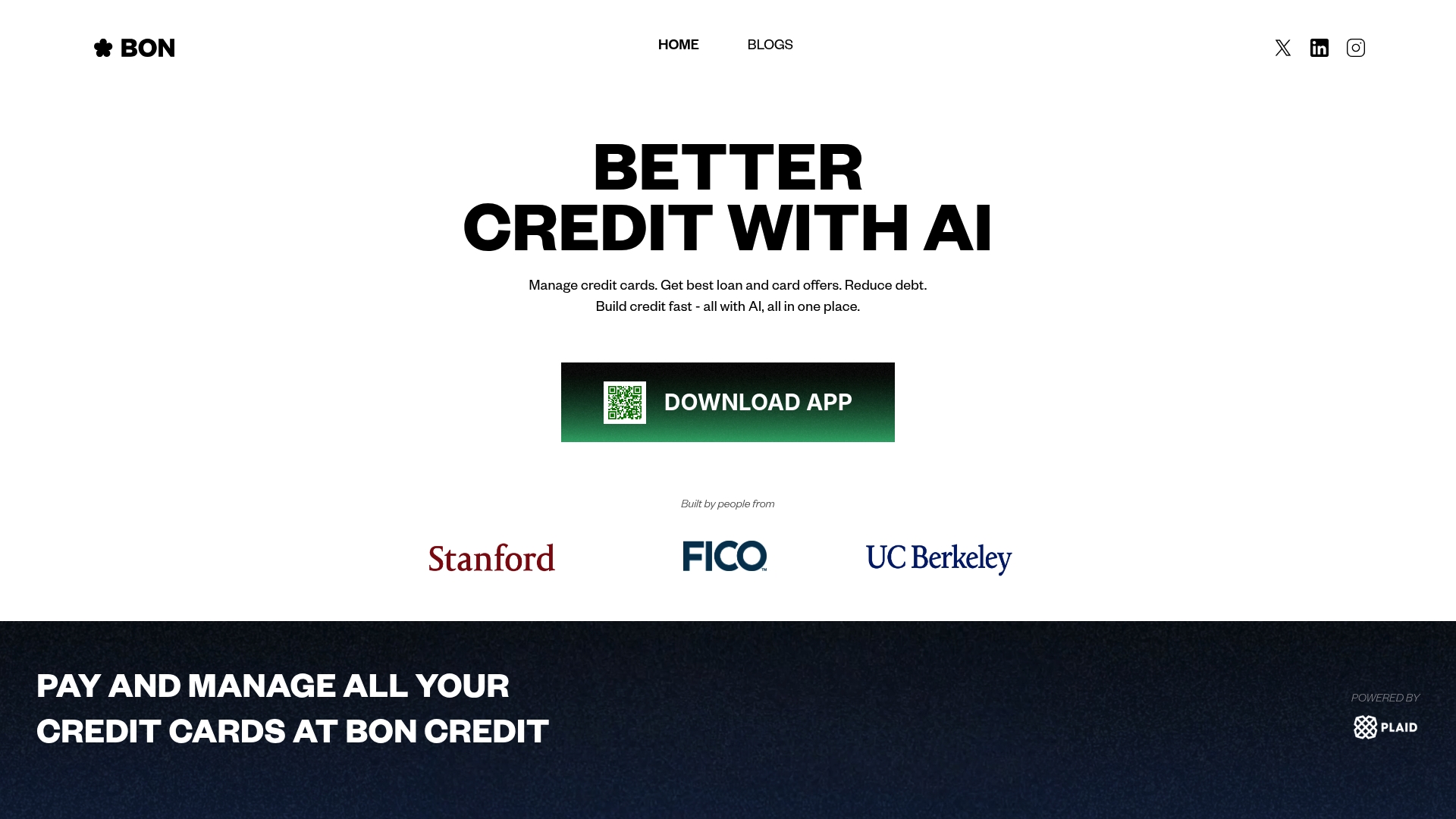

Bon Credit

At a Glance

Bon Credit tracks credit score factors and trends using soft pulls that do not affect your score. The app centralizes multiple credit cards and surfaces balance transfer and loan offers inside one interface. It also advertises automated bill payments and live alerts for inquiries and breaches.

Core Features

The app lets you manage multiple credit cards together and connect accounts through Plaid for account linking. It offers automated bill payment via ACH + Autopay and shows personalized card and loan recommendations. The platform monitors credit score drivers, sends alerts, and reports trends so you can act on potential issues quickly.

Key Differentiator

The vendor says the team includes people from Stanford, FICO, and UC Berkeley. That pedigree supports the app's emphasis on machine learning models for personalized recommendations. The result is an AI-driven, all-in-one approach to card management and credit offers rather than a single-purpose tracker.

Pros

Bon Credit groups card balances, payment dates, and offers in one place, which reduces manual tracking across issuers. The app supports major card networks and connects accounts through Plaid, which speeds setup and avoids manual entry. Automatic payment options and live alerts for inquiries and breaches help you react faster to fraud or missed payments, while the recommendation engine suggests credit upgrades and balance transfer options.

Cons

- Limited public detail on fees or subscription tiers, requiring direct inquiry before committing.

- Geographic availability is unclear, which may prevent access for some international or regional users.

- The vendor lists Plaid but does not publish a long list of supported banks or specific integrations.

- Statements about how fast scores improve and the depth of tracking are vague.

When It May Not Fit

If you need a fully transparent pricing page before signing up, this app may frustrate you. Companies or users who require guaranteed coverage for regional banks should verify access before full rollout. People who want audited certification details or exhaustive integration lists will likely find the public information sparse.

Notable Integrations

- Plaid for account linking and transaction access.

Who It's For

This app fits individuals who actively manage multiple credit accounts and want an integrated view of balances, due dates, and offers. It also serves people looking for automated payments and soft-pull monitoring that does not harm scores. Consumers who prefer an AI-driven recommendation layer for cards and loans will find the feature mix aligned to that need.

Real World Use Case

A user connects three credit cards through Plaid, enables ACH autopay for one card, and sets alerts for credit inquiries. The app flags a personalized balance transfer offer and shows how a transfer would change monthly interest costs. The user schedules the transfer and uses the alert history to confirm reduced utilization over time.

Website: https://boncredit.ai

Relief

At a Glance

Relief negotiates debt while keeping payments off the platform, with access granted through a membership fee. It covers credit card, personal loan, collection, and past due medical debt. Relief is not a lender or a debt collector and connects directly with creditors for negotiated outcomes.

Core Features

Relief runs debt reduction estimates and automated negotiation workflows and pairs those with debt payoff and transfer calculators. The platform offers credit score improvement guidance and legal response support for debt lawsuits. Personalized advice pulls from linked account data to make negotiation and repayment suggestions.

Key Differentiator

Relief centers on automated debt negotiation that does not route creditor payments through the app. That approach means the platform focuses on generating negotiation offers and repayment plans while members pay creditors directly. The model targets people who want negotiation tools without using a third party to collect funds.

Pros

The interface is easy to use, which lowers the barrier to starting negotiations and building a payoff plan. Negotiation tools can produce reduction offers and the system routes those offers to creditors rather than asking the user to send funds to Relief. Personalized advice and calculators help you see how offers affect payoff timelines and projected credit score changes. Core features work without a hard credit check, which keeps the process low friction for most people.

Cons

- Creditor cooperation is required, so outcomes vary and are not guaranteed.

- According to the company, responses to negotiation requests can take up to 60 days, which may slow progress for people who need quick results.

- The service has limited support for mortgages and auto loans, so large secured debts are out of scope.

- Linking accounts requires manual input, which introduces privacy risk if a user does not follow good security practices.

When It May Not Fit

If you need help with mortgages or auto loans, Relief currently does not cover those debt types. If you require fast, guaranteed settlements, that timeline may be too slow. If a creditor refuses to engage, the platform cannot force a resolution.

Who It's For

Relief fits individuals with unsecured debts such as credit card balances, personal loans, and medical bills who prefer a self service approach. It suits people willing to link account data to get tailored negotiation offers and a clear repayment plan. It also works for those who want to avoid credit checks while exploring reductions.

Real World Use Case

A member links credit card and medical debt accounts and runs the payoff calculators to compare scenarios. Relief generates negotiation letters and sends offers to creditors for review. The member accepts a reduction, pays the creditor directly, and adjusts the repayment plan to improve credit over time.

Pricing

Access to Relief requires a membership fee for the tools and insights. The platform does not collect negotiation fees or creditor payments; any settlement payments go directly to creditors.

Website: https://relief.app

Comparison of alternatives

Managing multiple credit accounts efficiently hinges on utilizing applications tailored to streamline financial monitoring and aid in strategic repayment planning. Among the featured solutions, Finja emerges as a distinctive contender with its integrative features, while other platforms demonstrate unique advantages in key areas.

AI integration for strategic payment recommendations

Finja's standout feature is its approach to credit management through daily AI-driven payment suggestions, which prioritize minimizing interest and preventing missed due dates. This view of all linked accounts addresses the needs of users juggling multiple credit cards but remains limited by its opaque pricing structure. In contrast, Bon Credit provides AI-powered personalized recommendations but also incorporates account monitoring and fraud alerts, making it suitable for users emphasizing security.

Automation capabilities and negotiation facilitation

Gauss Total Credit Manager significantly reduces the effort in managing debts by continuously automating balance transfers and debt negotiations. This approach eliminates the need for user intervention during refinancing or renegotiation processes, demonstrating a capability in this area. While Relief specializes in negotiation facilitation without routing funds through the platform, its reliance on creditor cooperation makes it less predictable.

Best fit

- Users managing several credit cards and requiring detailed centralized oversight will find Finja for its AI-driven daily payment guidance.

- Credit-savvy individuals prioritizing negotiation automations will benefit the most from Gauss Total Credit Manager.

- Global users seeking regional adaptability in banking integrations should consider Bon Credit based on its emphasis and feature scope.

- Those needing support for creditor communications while preferring independence in payment routing can rely on Relief's focused tools.

Our pick

For individuals seeking an intuitive solution combining financial overview consolidation with tailored, insights, Finja offers a notable advantage. Its unique combination of consolidated account visibility and AI-guided payment strategies excels for users managing multiple credit accounts. However, those prioritizing explicit pricing details or advanced automation in negotiations may explore other viable options like Gauss Total Credit Manager.

To identify the best platform for managing your multi-card credit accounts while optimizing payments and interest, consider the following comparison:

| Platform | Core Feature | Key Differentiator | Pricing | Notable Limitation |

|---|---|---|---|---|

| Finja | Consolidated balances with AI payment recommendations | Integrated AI-driven payment logic | Price not published | Limited transparency on subscription pricing |

| Gauss Total Credit Manager | AI-driven debt negotiation and balance transfers | Persistent negotiation without manual effort | $4.99/month | Limited free features |

| Bon Credit | Credit trends with soft pulls and account integration | Machine learning for personalized credit recommendations | Price not published | Geographic availability uncertainty |

| Relief | Automated debt negotiation for payoff and reductions | Self-service creditor negotiation | Membership fee applies | Creditor cooperation required; outcomes not guaranteed |

Struggling to Manage Multiple Credit Cards Efficiently?

Many people with two or more credit cards find it hard to track balances, due dates, and payment priorities. Finja provides a clear view of all your credit cards in one place, paired with AI-powered recommendations that suggest which payments to make and when. This helps reduce interest costs and avoids missed minimum payments.

If you want personalized payment guidance that looks at your whole credit picture, explore Finja's AI-powered platform. Take control of your credit health with a consolidated balance snapshot and daily payment suggestions tailored for you. See how you can prioritize your payments and set spending limits by category for better financial control at Finja.

FAQ

How does Finja help reduce credit card interest costs?

Finja offers AI-powered payment recommendations that suggest amounts and timings to reduce interest. The app shows consolidated card balances and adapts suggestions based on these balances and payment schedules. This feature allows users to more effectively manage their debt and lower avoidable interest costs.

What is the difference between Finja and Gauss Total Credit Manager?

Gauss Total Credit Manager excels in automated debt negotiation, requesting lower interest rates and improved terms on behalf of users. Finja, on the other hand, provides AI-driven payment guidance tailored to minimizing interest from a consolidated view of all cards. Users who prefer a hands-on approach to negotiate rates might find Gauss more suitable.

Which platform provides the best overall overview of credit cards?

Finja generates a full credit overview in one place, enabling users to view multiple card balances easily. This feature contrasts with other platforms that may not integrate all accounts into one dashboard, making tracking due dates and payment recommendations more straightforward for users.

Can I set spending limits with Finja?

Yes, Finja allows users to set spending limits by category, such as dining and shopping. This feature helps maintain control over expenses, preventing overspending and promoting healthier credit management practices.

How does Finja personalize recommendations for users?

Finja uses AI to deliver personalized payment suggestions based on linked card balances and user spending behavior. This targeted approach ensures that recommendations are relevant and actionable, helping users manage credit effectively.