Credit card cycling is defined as maxing out your credit card, paying it off, and then charging it to the limit again within the same billing cycle. This practice is distinct from simply making multiple payments, and American Express warns that issuers can flag it as problematic even when payments arrive on time. Understanding how credit card cycling works protects your account standing, your credit score, and your ability to use credit when you actually need it. This guide breaks down the billing cycle mechanics, the real difference between cycling and smart payment strategies, and what you should do instead.

How does the credit card billing cycle work?

A billing cycle lasts about 28–31 days, starting the day after your previous statement closes. Every purchase, fee, and credit that posts during those days accumulates until the closing date. The closing date is the snapshot moment. It locks in your statement balance and determines what gets reported to the credit bureaus.

The payment due date falls about 21–25 days after the closing date. That window is your grace period. Pay the full statement balance within that window, and you owe zero interest on purchases. Miss it or pay only the minimum, and interest starts accruing on the remaining balance.

One detail that trips up many cardholders: the closing date and the due date are not the same thing. Citi notes that confusing these two dates is one of the most common causes of unexpected interest charges. The closing date locks your balance. The due date is your deadline to pay it.

Purchases you make after the closing date do not appear on the current statement. They roll into the next billing cycle. This timing detail matters a great deal when you are trying to manage what balance gets reported to the bureaus each month.

- Closing date: The last day of your billing cycle. Your statement balance is set here.

- Statement balance: The total you owe as of the closing date, including any prior balance.

- Payment due date: Roughly 21–25 days after closing. Pay in full to keep your grace period.

- Grace period: The interest-free window between closing date and due date. It only applies if you carry no prior balance.

Pro Tip: Set a calendar reminder two days before your closing date. A payment made before closing reduces the balance that gets reported to the credit bureaus, which can lower your reported utilization that month.

What is credit card cycling, and how does it differ from smart payments?

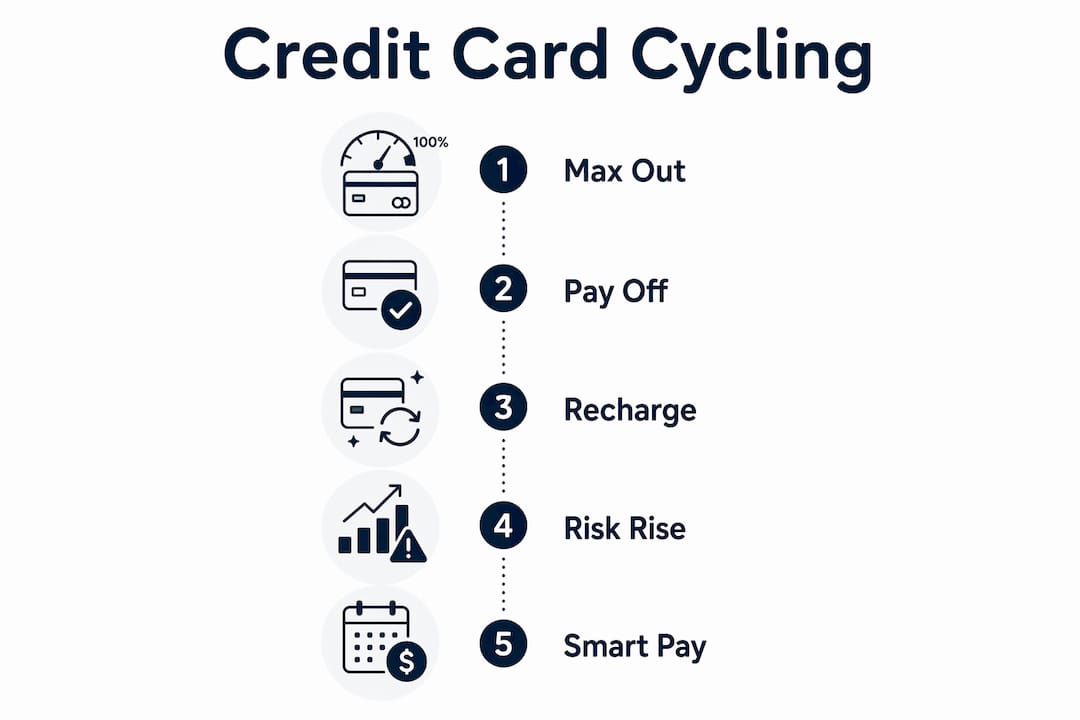

Credit cycling is the behavior of maxing out a credit card, paying it off, and then maxing it out again within the same billing cycle. Think of a card with a $5,000 limit. You charge $5,000, pay it off mid-cycle, and then charge another $5,000 before the closing date. You have now cycled $10,000 through a $5,000 limit in a single cycle.

This is not the same as making two payments in one month to keep your balance low. Those are two very different behaviors with very different consequences.

Here is how to tell them apart:

- Multiple payments to reduce utilization. You charge $2,000 on a $5,000 card, pay $1,500 before the closing date, and carry a $500 balance into the statement. This is a legitimate payment strategy that lowers your reported utilization.

- Early payoff before the due date. You pay your full statement balance a week before the due date. This preserves your grace period and costs you nothing extra.

- Credit cycling. You charge $5,000, pay it off, charge another $5,000, and pay that off too, all before the closing date. The total spending far exceeds your credit limit within one cycle.

The key distinction is whether your total spending within a cycle exceeds your credit limit. If it does, you are cycling. If it does not, you are simply managing payments well.

Capital One notes that mid-cycle payments alone do not restart your grace period if you are carrying a balance from a prior cycle. Grace period protection depends on paying the full prior statement balance by the due date. Making extra payments mid-cycle is fine. Cycling is not.

Pro Tip: Track your total monthly spending against your credit limit, not just your current balance. If your spending is approaching double your limit within one cycle, you are in cycling territory.

What are the risks of credit card cycling?

Credit cycling patterns can be viewed by issuers as higher risk behavior that may trigger account suspensions or credit score impacts. That is the core danger. Even if every payment arrives on time, the pattern itself raises red flags.

"Credit cycling can be flagged by issuers as problematic even if payments are made on time." — American Express

Issuers use transaction monitoring to detect unusual patterns. Repeatedly maxing and paying off a card signals that you may be using the card as a short-term loan or running a business through a personal account. Neither is what personal credit cards are designed for.

The specific risks include:

- Account suspension or closure. Issuers can close accounts they consider high risk, even with no missed payments.

- Credit limit reductions. An issuer may cut your limit without warning, which spikes your utilization ratio overnight.

- Credit score damage. A sudden limit cut or closed account raises your utilization and shortens your credit history, both of which hurt your score.

- Loss of rewards or benefits. Some issuers will claw back points or miles if they determine the account was misused.

- Fraud flags. Rapid cycling can trigger fraud detection systems, freezing your card at the worst possible moment.

The irony is that cardholders who cycle often do so thinking they are managing their utilization well. The reality is the opposite. Aggressive cycling to manipulate utilization can backfire, as issuers may treat the behavior as risky, impacting credit or account standing.

How to manage credit card payments without cycling risks

The most effective credit card payment strategy is built on knowing your closing date and paying your full statement balance by the due date. Everything else flows from those two habits.

| Strategy | What it does | Cycling risk |

|---|---|---|

| Pay full statement balance by due date | Preserves grace period, avoids interest | None |

| Pay before closing date to cut utilization | Lowers balance reported to bureaus | None if spending stays under limit |

| Make multiple mid-cycle payments | Reduces running balance, no grace period reset | None |

| Max out, pay off, max out again | Cycles spending beyond credit limit | High |

TD Bank notes that timing benefits come from the balance at the statement closing date, not from mid-cycle payments. A payment made two days before closing is far more effective for utilization than one made the day after. That single insight changes how you schedule payments.

Paying the full statement balance by the payment due date preserves your grace period and helps you avoid interest charges on purchases entirely. Paying only the minimum allows interest to accrue on the remaining balance, and that interest compounds quickly.

Billing cycle timing is a practical lever for credit management. Knowing when purchases post can help you manage credit utilization and keep your balance under control without ever touching cycling territory. Tools like Myfinja are built specifically to help cardholders track these dates across multiple cards and act before the closing date, not after.

Key takeaways

Credit card cycling is defined as spending beyond your credit limit within a single billing cycle by paying off and recharging the card repeatedly, and it carries account and credit score risks that outweigh any perceived benefit.

| Point | Details |

|---|---|

| Cycling exceeds your limit in one cycle | Charging, paying off, and recharging past your limit in one cycle is cycling, not smart payment management. |

| Closing date drives bureau reporting | The balance on your closing date is what gets reported; pay before it to lower utilization. |

| Grace period requires full balance payoff | Paying only the minimum or carrying a balance eliminates your interest-free window. |

| Issuers can act without warning | Account closures, limit cuts, and fraud flags can follow cycling patterns even with on-time payments. |

| Multiple payments are safe if spending stays under limit | Making two or three payments per cycle is fine as long as total spending does not exceed your credit limit. |

Credit cycling: more risk than most cardholders realize

I have spent years watching cardholders make the same mistake. They discover that paying their card off mid-cycle frees up available credit, so they do it again and again, convinced they are being financially disciplined. What they are actually doing is cycling, and they have no idea until the issuer acts.

The part that frustrates me most is how preventable it is. The billing cycle is not complicated. A 28 to 31 day window, a closing date, a due date. That is the whole structure. But most cardholders never learn it in any formal way, so they operate on instinct and end up in trouble.

My honest opinion: cycling is almost never worth the risk. The cardholders who benefit from it are running very specific cash flow strategies, and even they are playing with fire. For the average person managing one to three credit cards, the downside of an account closure or a limit cut is far worse than any short-term cash flow benefit cycling provides.

The smarter path is to know your closing date, pay before it when you want to lower utilization, and pay the full statement balance by the due date every single month. That combination costs nothing, protects your grace period, and keeps your issuer from ever looking twice at your account.

— Thiri

Myfinja helps you stay ahead of your billing cycles

Managing multiple credit cards means tracking multiple closing dates, due dates, and utilization ratios at once. Missing one date can cost you interest or trigger a utilization spike that hurts your credit score.

Myfinja is an AI-powered credit card coach that monitors your billing cycles, flags the right time to make payments, and helps you avoid the patterns that put accounts at risk. Instead of guessing when to pay, you get clear guidance based on your actual card data. Cardholders who want to reduce interest costs and protect their credit health can start with Myfinja and get a clearer picture of where their payments stand right now.

FAQ

What is credit card cycling?

Credit card cycling is when you max out a credit card, pay it off, and then charge it to the limit again within the same billing cycle. American Express identifies this as a behavior that issuers can flag as high risk, even when payments are on time.

How does the credit card billing cycle work?

A billing cycle lasts 28–31 days and ends on the closing date, which locks in your statement balance. Your payment is due about 21–25 days after that closing date.

Does making multiple payments per month count as cycling?

No. Making two or three payments per month is not cycling as long as your total spending does not exceed your credit limit within the cycle. Cycling only occurs when you charge beyond your limit by paying off and recharging repeatedly.

Can credit card cycling hurt your credit score?

Yes. Issuers can respond to cycling patterns by reducing your credit limit or closing your account, both of which raise your utilization ratio and damage your credit score.

What is the safest way to lower credit utilization?

Pay down your balance before your statement closing date. The balance reported to the credit bureaus is the one on your closing date, so a payment made before that date directly reduces your reported utilization.